Board the legitimate merchants and shut the fakes out before first settlement.

Read every application across signals a fake merchant cannot fabricate, and carry that trail into monitoring on the same record once the merchant boards.

Move every applicant from form to monitored merchant.

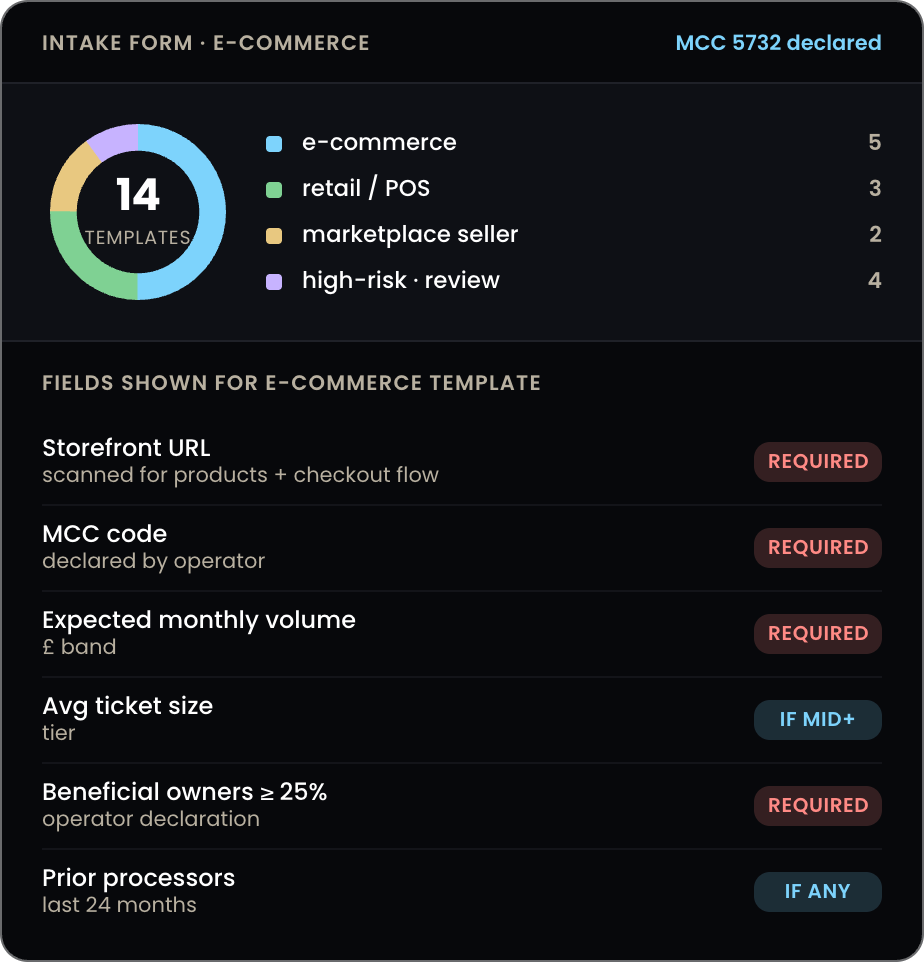

Collect only what each merchant type needs.

Adapt the form to the merchant's structure and jurisdiction so the applicant types only what their case requires. Pre-populate the company fields from the registry and let the operator upload the rest in minutes.

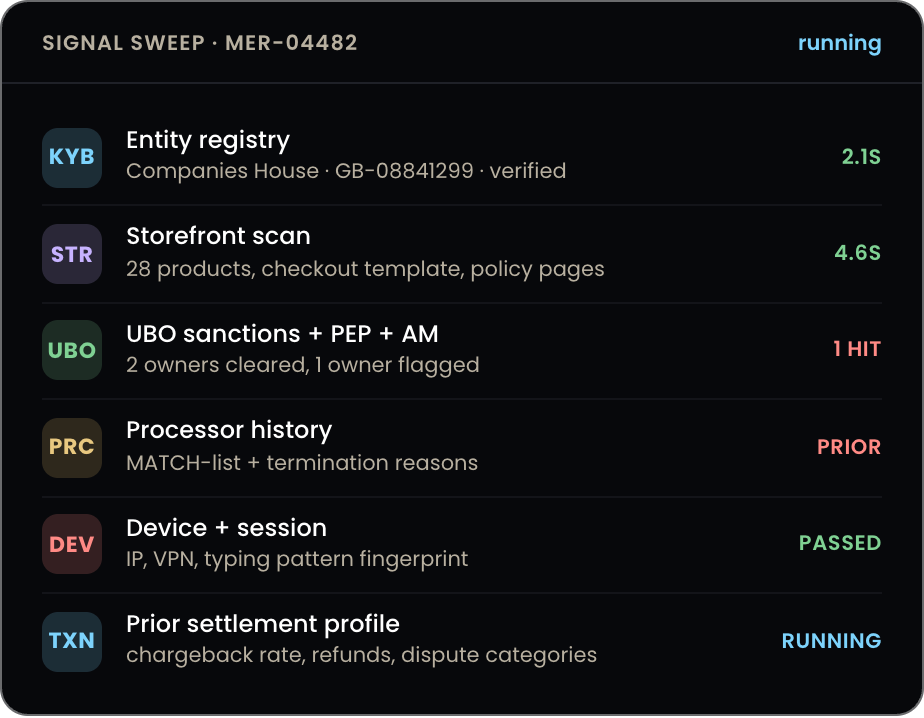

Fire the full signal sweep the moment the form submits.

Trigger the storefront scan, MCC validation, ring detection, identity, sanctions, and device read in parallel, so a complete picture of the merchant sits ready before an analyst opens the case.

Score every merchant and route the case from one number.

Drive routing from a single merchant risk score, so clean SMBs hit auto-approval while elevated cases go to EDD and prohibited categories reject without an analyst touching the file. Tune every threshold in the console and let each change log against the rule version for examiner replay.

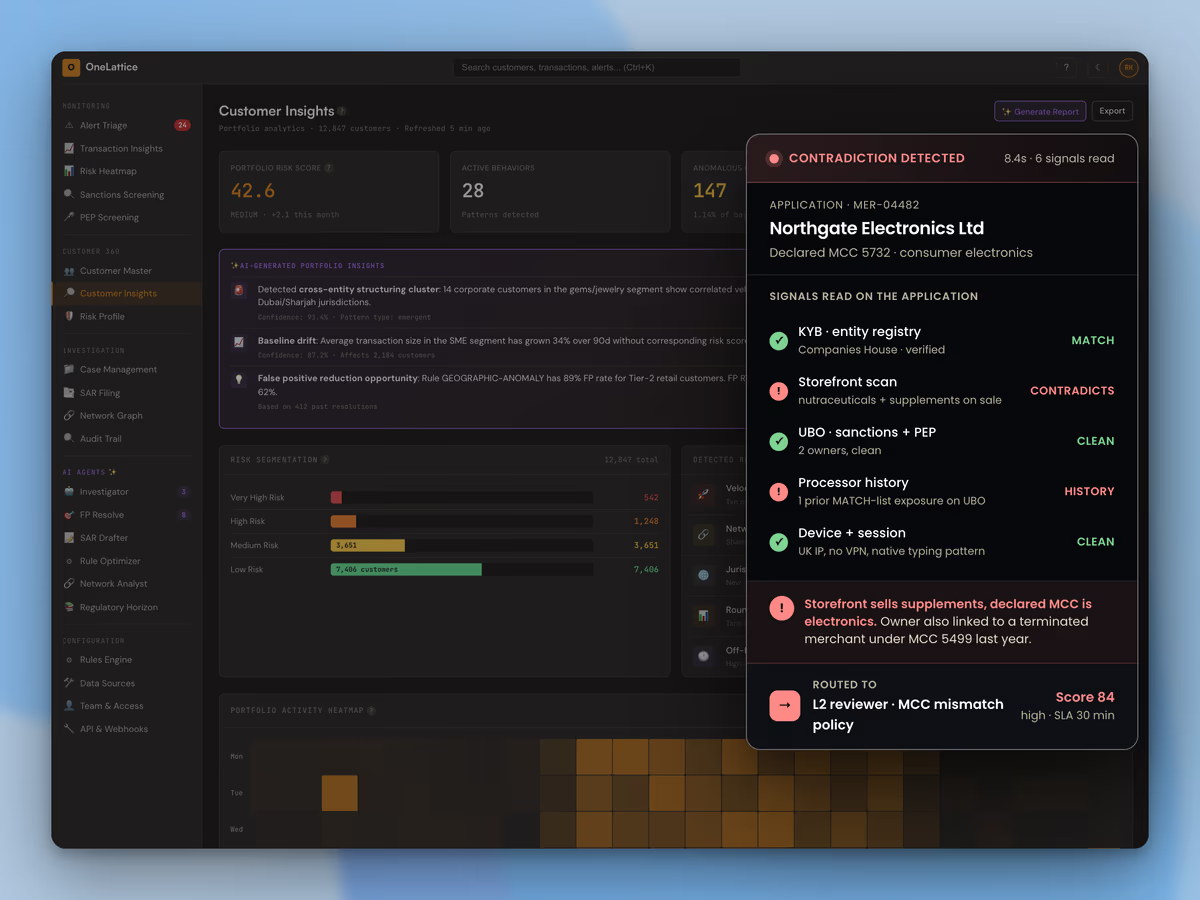

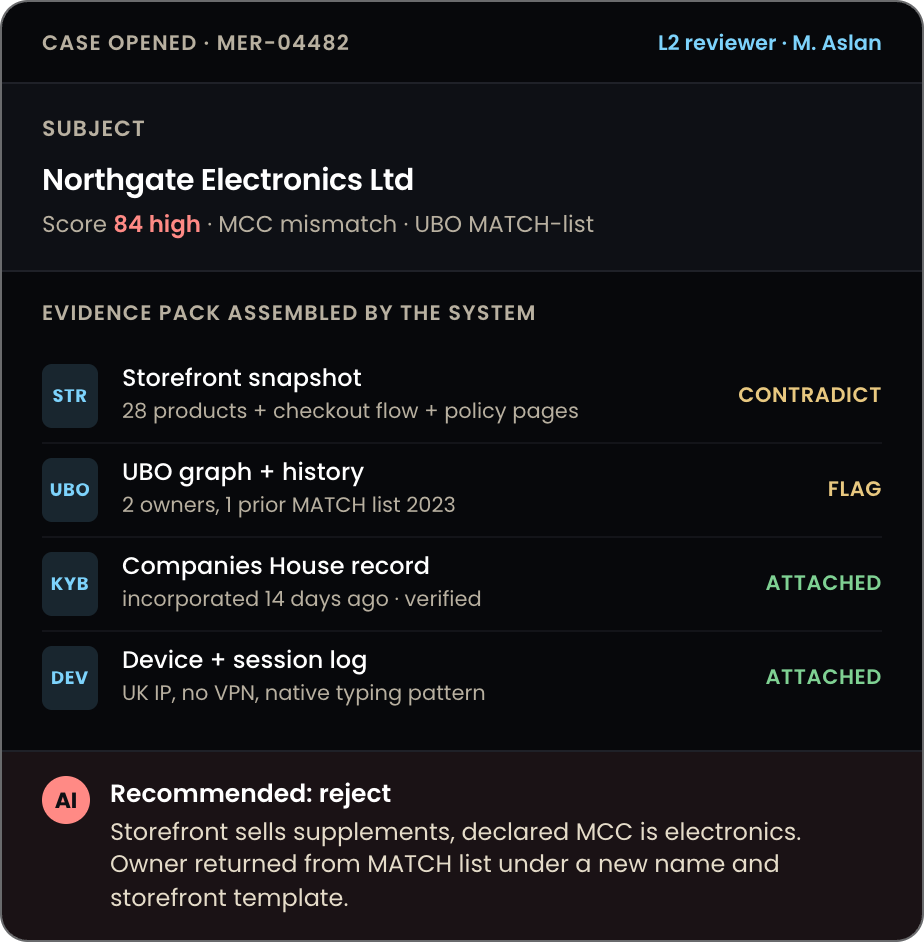

Open every escalation with the case already assembled.

Hand the analyst a file with the registry, storefront, UBO exposures, device graph, and processor history already compiled, plus a recommended decision. Approve, reject, or send an RFI, and let each action log a reason code against the rule version.

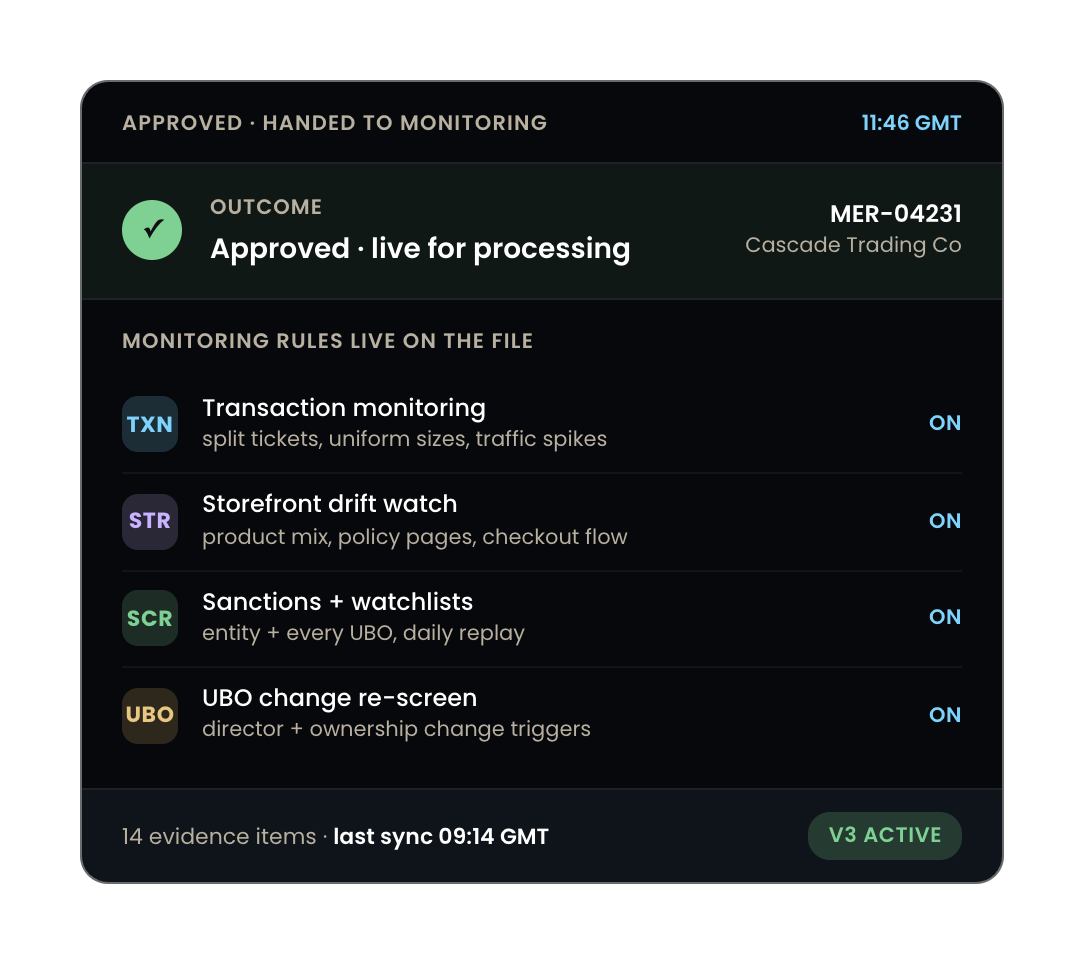

Carry the approval into monitoring on the same record.

Treat the approval as the merchant's monitoring baseline. The MCC, the storefront snapshot, the UBO list, the processor history, and the risk score follow the merchant into transaction monitoring and periodic review, so any drift raises an alert against the same record that booked the merchant.

SIGNAL SURFACE

Surface the forgery before the team ever approves.

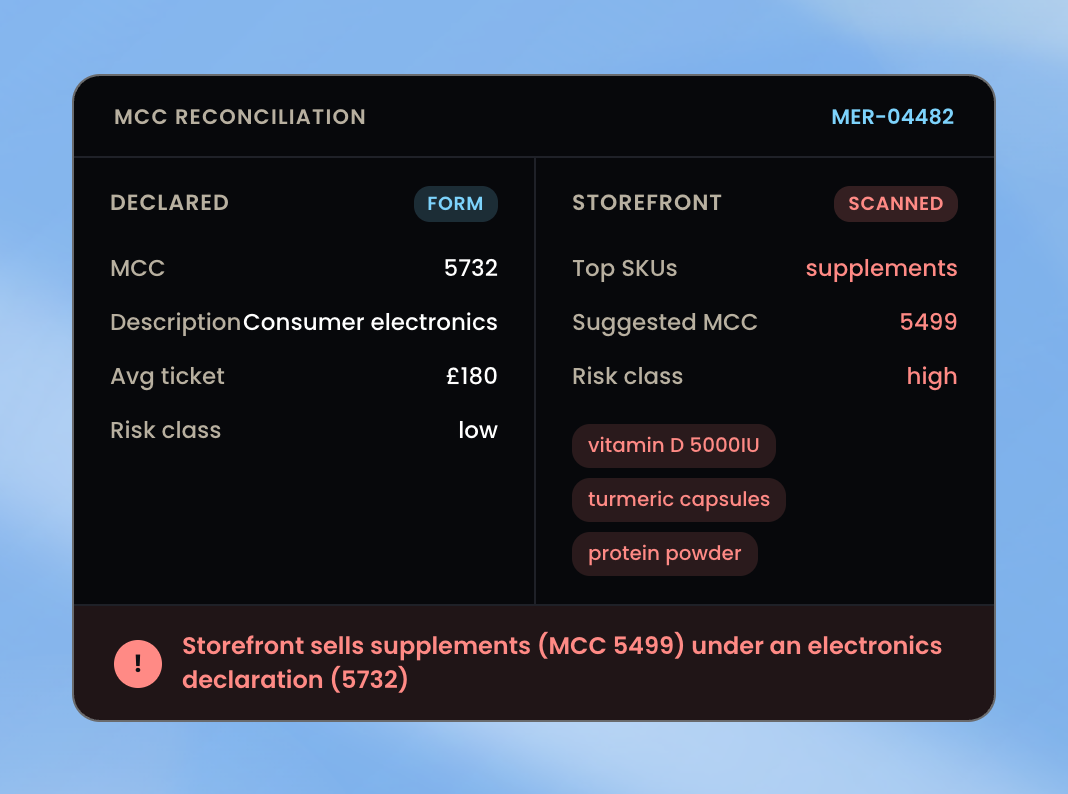

Cross-check what the merchant declares against the evidence the application actually carries, so a recycled owner or a cloned storefront fails the moment a separate signal contradicts the file.

Verify the business against the registry, the licensing record, and the activity actually visible on the storefront, so a declared MCC has to match what the operator sells.

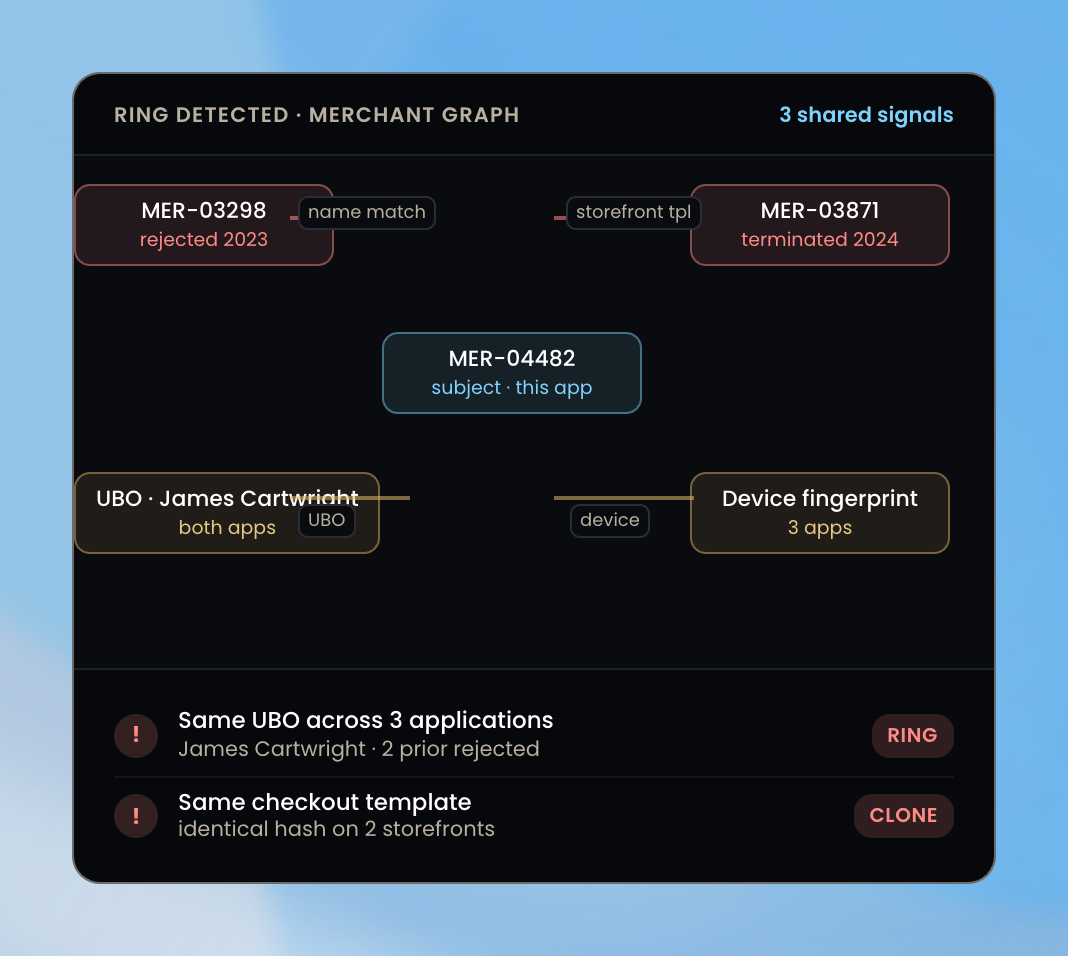

Scan the storefront for the products on sale, the checkout flow, and the templates behind it, and flag any clone tied to an applicant the team has already rejected.

Run identity, sanctions, PEP, and adverse-media checks on every beneficial owner, and link the result back to any prior rejection where the same person appears.

Merchant Risk Graph

Pull the merchant's prior processor history into the file, including the termination reason codes and any MATCH-list exposure that follows the owner across processors.

Capture the device and the application session, and watch for shared fingerprints, VPN routing, and the typing patterns that mark a coached or recycled applicant.

Bring prior processing data into the application, so an analyst sees the chargeback trend, the refund pattern, and the dispute categories before the new account opens.

Read the signals paperwork cannot fake.

See the mechanism behind every decision.

Replay the validation, the graph link, and the rule version behind any approval the moment an examiner asks for it.

POST-ONBOARDING

Watch every approved merchant for drift.

MCC drift

Watch the product catalog drift away from the approved MCC, and route the diff to the assigned analyst the moment the merchant edges into a higher-risk category.

Transaction laundering

Catch processing patterns that contradict the stated business, so split tickets, uniform ticket sizes, and traffic spikes the storefront cannot explain raise an alert against the same merchant record.

UBO change

Re-screen every new beneficial owner the moment a registry update lands, and auto-escalate the case if the new name crosses a sanctions, PEP, or adverse-media threshold.

Storefront content change

Rescan the storefront the moment the operator changes the product mix, the policy pages, or the checkout flow, and flag any swap into a prohibited category against the approved baseline.

Sanctions re-screening

Replay every watchlist update against the entity and every UBO, and tune the hit logic and review routing per jurisdiction so each market handles the alert the way local compliance expects.

Cross-merchant device collusion

Catch device fingerprints shared across two or more merchants in the portfolio, group the linked accounts as a ring candidate, and hand the investigation an entity view that already maps the connections.

Agents on this workflow.

OneLattice's purpose-built agents that handle this work end-to-end.

EDD Agent

Researches the business and every UBO across registries, filings, and corporate documents, and feeds the analyst a dossier the team would otherwise spend a day building.

Screening Analyst

Runs sanctions, PEP, and adverse-media checks against OneLattice's GraphIntel and writes the result straight into the case file.

Entity Resolver

Unifies aliases, transliterations, and near-matches into a single entity view, so a recycled owner under a new name surfaces against the same record.

Network Analyst

Maps rings, mule networks, ownership obfuscation, and multi-accounting across the portfolio, so the analyst sees the graph the moment a name returns.

PLATFORM

Take the same stack across the rest of the merchant lifecycle.

One platform from boarding through monitoring.